How to Start and Grow a Real Estate Business: Essential Steps and Tips

This guide outlines steps for starting & growing a successful real estate business in India. Learn how to navigate the market & avoid common pitfalls.

Let’s face it—the thought of starting a real estate business sounds as scary as it is exciting. On one hand, you’re stepping into one of the most rewarding industries in India, with endless potential for growth. On the other hand, you might be wondering where even to begin.

The good news? You don’t need to have it all figured out from day one. There’s a step-by-step approach that can help you build a strong foundation and guide you through each critical phase. This blog will outline the essential steps and share tips on starting and growing your real estate business in India.

Understanding Real Estate Business

Real estate is one of the most lucrative business sectors in India. It involves buying, selling, managing, or investing in properties, which can include residential, commercial, industrial, or even agricultural land.

The real estate sector in India has been growing significantly. This growth can be attributed to several factors, including rapid urbanisation, population growth, and increased demand for housing and commercial spaces. Additionally, government initiatives like “Housing for All” and smart city projects have boosted investor confidence and made the sector more accessible.

When it comes to numbers, the future looks incredibly promising. India’s real estate sector is projected to reach US$ 5.8 trillion by 2047. It is expected to contribute around 15.5% to the country's GDP, compared to its current share of 7.3%.

With such expansion ahead, the opportunities in the sector seem to be endless. This opens up vast possibilities for entrepreneurs aiming to establish a profitable and sustainable business in this ever-growing market.

How to Start and Grow Your Real Estate Business?

Starting a real estate business requires careful planning and strategy. It all begins with a spark of motivation, a lot of research, and a good grasp of the market. A well-crafted plan will give you a solid foundation, help you prepare for harsh market conditions, and set clear goals for sustainable growth.

Before we outline the steps, remember that real estate is a long-term game that requires a lot of patience and persistence.

1. Research and Understand the Market

Before starting your real estate business, it is essential to thoroughly research and understand the market you’ll be operating in. This foundational step will help you identify opportunities, avoid costly mistakes, and make smart decisions right from the start. Here are key areas to focus on:

Market Trends: Keep an eye on current real estate trends in your area, such as property prices, demand for specific types of properties (residential, commercial, etc.), and upcoming developments. This will give you a sense of the market’s direction.

Local Demand: Get a clear picture of who's buying in your area. Are young families moving in? Are investors active? Maybe there's a growing demand for student housing. Understanding local demand helps you tailor your services and marketing to the right audience.

Competition: Analyse your competitors—what niches are they focusing on, how do they price their properties, and what strategies are they using to attract clients? This will help you identify gaps in the market and opportunities to differentiate your business.

Legal and Regulatory Landscape: Familiarise yourself with the local real estate laws and regulations. This includes zoning laws, building codes, and government initiatives like RERA (Real Estate Regulatory Authority) in India. Staying compliant is crucial to avoid fines and penalties.

Economic Conditions: Pay attention to broader economic factors such as interest rates, inflation, and government policies. These can directly affect property values and buyer behaviour. Additionally, assess the overall health of the economy. How stable is the job market? What's the average household income? A strong economy usually means a healthy real estate market.

Infrastructure Development: Look at current and planned infrastructure projects. New metro lines, schools, universities, or malls can significantly boost property values and demand. For example, better public transport and nearby universities can drive up demand for student housing.

The knowledge you gain from this research will help you craft a business plan that is realistic, data-driven, and aligned with the opportunities in your area.

2. Create Your Business Blueprint

This stage will lay the groundwork upon which you will eventually build your comprehensive business plan. It’s about making important choices regarding your business direction and figuring out how you want to be involved. Here's how to start:

Craft Your Ideal Personal Plan

Your personal plan should reflect your goals, financial aspirations, and the time you’re willing to invest. Answer questions like:

Where do you see yourself in 5-10 years in the business?

How many hours are you prepared to work each week?

Do you prefer high-risk, high-reward projects or safer, more predictable ventures?

How much money do you want to earn?

What tasks will you handle personally, and which ones will you delegate or outsource?

The goal is to find your ‘why.’ Sure, money is a driving factor, but look deeper—what’s the real motivator that fuels your passion? Understanding this will keep you focused and resilient through the challenges.

Choose Your Niche

Choose a niche that aligns with your strengths and interests. Focusing on a specific area of real estate will give you time to become an expert, cater to the needs of a targeted audience, and stand out in the market. Here are a few popular niches you can consider:

Residential Real Estate

Commercial Real Estate

Luxury Properties

Resort and Vacation Rentals

Condos

Property Management

Pick a niche that plays to your strengths and where you believe you'll excel. It's best to focus on one, or at best two, areas to start. Trying to cover everything right away isn’t practical.

Identify Your Audience

The importance of this step cannot be stressed enough. To reach the right people, you must know exactly who they are. Understanding your audience will shape every aspect of your business, from your marketing strategy to the services you provide.

For example, marketing to students looking for hostels is very different from targeting young professionals seeking co-living spaces. Each group has unique pain points, concerns, desires, and goals. So, take the time to develop detailed profiles of your ideal clients and craft a buyer persona by researching factors such as:

Age range and generation (Millennials, Gen X, Baby Boomers)

Income levels and purchasing power

Family status (single, married, with children)

Professional background

Lifestyle preferences and priorities

Common pain points

Once you have a clear understanding of your audience, you can tailor your services to meet their specific needs. Remember, the more precisely you define your audience, the more effectively you can serve them.

Choose a Legal Business Structure

The legal structure of your real estate business plays a crucial role in your operations, taxes, and personal liability protection. In India, there are several business structures to choose from, each with its own advantages and drawbacks. Here are the most common options:

Sole Proprietorship: This is the simplest structure, where you own and operate the business alone. It's easy to set up, but you’re personally liable for any debts or legal issues.

Partnership: This means you will have one or more partners sharing ownership, responsibilities, and profits in the business. Each partner is personally liable for the business’s debts and obligations.

Limited Liability Company (LLC): An LLC offers the benefit of limited liability protection, meaning your personal assets are protected from business debts.

Private Limited Company (Pvt Ltd): Ideal for larger businesses, this structure allows you to raise funds by selling shares and offers limited liability protection. However, it comes with more regulatory requirements.

Before choosing your business structure, consider factors like the liability protection you need, your long-term business goals, and how the structure will impact your ability to attract investors or secure financing.

Also, hire legal and accounting professionals to guide you through this important decision. This will help you avoid costly mistakes and ensure compliance with regulations.

3. Create a Robust Business Plan

Once you’re done with the research and initial planning, it’s time to put your plan on paper—or on your computer, whichever you prefer. A well-structured business plan acts as a roadmap, guiding you through each stage of your venture and helping you stay focused. Here’s what to include:

Executive Summary: A brief overview of your business, its objectives, and your vision for the future. This should summarise the key elements of your plan. (This section often determines whether someone keeps reading.)

Company Overview: Outline your business structure, mission statement, the niche you’ve chosen, and your target audience.

Risk Assessment: Identify potential challenges your business may face, such as market fluctuations or regulatory changes, and how you plan to mitigate them.

Marketing and Sales Plan: Detail your strategies for attracting clients and closing deals. Include both online and offline marketing tactics, social media plans, and sales approaches.

Progress Reporting: Establish how you will track the progress of your business goals, key performance indicators (KPIs), and timelines for achieving milestones.

Team: If applicable, outline the structure of your team, including roles and responsibilities. Mention whether you'll hire staff or work with partners and what skills are essential.

Budget: Provide a detailed breakdown of your projected expenses, including startup costs, operating expenses, and marketing budgets.

Finance: Include your financial projections, revenue models, and cash flow forecasts. If you’re seeking funding, specify the amount you need and how you plan to use it.

A well-crafted business plan not only helps you clarify your vision and strategy but also plays a crucial role in securing financing from investors or lenders. This plan is not set in stone. You can revisit and revise it as your business grows and the market changes.

4. Assess and Get Your Finance

Get a clear understanding of your finances—how much you’ll be earning and how you plan to spend it. This clarity will help you plan how to secure funding for your startup or finance its growth down the line. Here’s how to go about it:

Understand Your Expenses: Think beyond startup costs. Factor in ‘carrying costs’, which include the money you’ll need to cover your living expenses for the first few months as you establish your business.

Estimate Revenue Projections: What’s your potential income? Is it through sales commissions or rental income? Knowing your expected cash flow will help you make informed decisions about budgeting and investments.

Manage Cash Flow: Set up a system to handle market fluctuations. Track income and expenses to stay stable, even during slow periods.

Create a Contingency Fund: Prepare for unexpected costs by setting aside a financial cushion to handle surprises like market downturns.

Once you have a clear picture of your financial needs, look for funding options that align with your business plan. You can consider bank loans, investors, or government schemes to support your growth.

5. Get Required Licenses & Certifications

Starting a real estate business in India requires specific licenses and certifications to operate legally.

Begin by registering your business with your state’s Real Estate Regulatory Authority (RERA). Then, you’ll need a real estate agent license, a GST number, and service tax registration.

If you plan to work alone, you’ll also need to file your Income Tax Returns and provide the necessary documents for RERA registration. You can work with a consulting firm to help you navigate the licensing process. They can assist with the paperwork and ensure you don’t miss any steps.

6. Secure the Right Insurance Coverage

Insurance will safeguard your business and provide peace of mind against unforeseen events. Here are some key types of insurance you should consider:

Professional Indemnity Insurance: Protects you from claims made by clients for negligence or errors in your professional services.

Property Insurance: Protects your properties from damage caused by fire, theft, or natural disasters. It covers repair or replacement costs.

Public Liability Insurance: Provides coverage for legal claims if a third party suffers injury or property damage on your premises.

Workers' Compensation Insurance: Covers medical costs and compensation for employees in case of work-related injuries.

Remember, most real estate transactions involve large sums of money, so having the right insurance coverage is essential to protect your investment and minimize risks.

7. Develop a Sales Strategy

Having a well-defined sales plan is vital for converting leads into clients and driving revenue in your real estate business. Here’s a breakdown of each crucial component of sales:

Prospecting: Start by identifying potential clients through various channels like referrals, social media, local community forums, or real estate websites. You can use platforms like Magic Bricks, 99acres and Housing.com to find leads and connect with buyers or sellers in your area.

Lead Generation: Use online ads, social media, and email marketing to generate interest. Building a strong online presence with targeted content will help attract the right audience and create a steady flow of leads.

Lead Nurturing: Once you’ve got leads, it’s crucial to stay in touch. Use CRM tools to send personalized follow-ups, offer helpful resources, and keep them engaged until they’re ready to take the next step. Consistent communication builds trust and moves leads closer to becoming clients.

To turn this strategy into tangible results, keep an eye on the data. Track key metrics like conversion rates, response time to inquiries, lead sources, and engagement levels to optimize your strategy.

8. Build Your Brand Identity

In a crowded real estate market, simply having knowledge and experience isn’t enough. Standing out requires a strong brand identity that reflects who you are and what sets you apart.

Craft Your Brand Essentials

First, define what your brand stands for. Think about your unique value proposition and what makes you different from the competition. Accordingly, develop a distinctive identity that speaks to your target audience:

Choose a memorable business name that reflects your values and specialization

Design a professional logo and consistent visual elements (colors, fonts, imagery)

Craft a compelling brand story that explains your unique value proposition

Develop a clear brand voice and messaging that connects with your target market

Define your core values and make sure they shine through in all interactions

A well-crafted brand will build credibility and keep your business fresh in the minds of potential clients. This will make it easier for people to remember and recommend you when the need arises.

Define Your Unique Selling Proposition (USP)

To create your USP, start by considering the needs of your target audience and think about how you can meet them better than your competitors. For example, if you specialize in student housing, you might offer convenient payment options, while your USP in selling properties could focus on luxury high-rise apartments. Your USP will define your marketing strategy.

9. Create a Marketing Strategy

Once you've established your brand identity, the next step is to create a marketing strategy that helps you reach your target audience. A well-executed marketing plan will ensure your brand gets visibility, attracts clients, and generates leads. Here's how to build a comprehensive marketing strategy:

Design a Professional Website And Optimize For SEO

Nearly 43% of tenants use real estate websites to search for a home. So, you need to have a good website to attract online leads.

The website must be user-friendly, mobile-responsive, and fast-loading. It should clearly showcase your services, property listings, and client testimonials.

Make sure the website is optimized for SEO so it ranks well in search engines. This will ensure potential clients find you over your competitors. Include clear contact information and a call-to-action that encourages visitors to get in touch or explore your listings.

You can also start a blog section to share market insights and property tips. Write blogs with relevant keywords and ensure that each page is crawlable by Google. This will help you build authority and improve search engine rankings.

To boost your local SEO, set up a Google Business Profile. It’s a straightforward way to help nearby clients discover you and keep your business at the forefront.

Get Active on Social Media

As the famous business leader Richard Branson said, "Social media is not just a trend; it’s the way our society communicates. Your business needs to be part of that conversation."

In today’s digital age, social media is where your clients spend their time. So, your business must have a strong presence on platforms like Facebook, Instagram, LinkedIn, and X (Twitter).

Post regularly to engage your audience with short videos, virtual tours, and property photos. Use this as a medium to share your brand's story and values. Actively respond to comments and questions to build a community around your brand.

Work on Personal Branding

Your personal brand is just as important as your company's brand. Personal branding helps humanize your business and acts as a bridge between you and potential clients. After all, real estate is a people's business.

You can build your brand by showcasing your expertise on LinkedIn, attending industry events and conferences, and hosting live events. When done right, personal branding will increase your trust and authority, which in turn will benefit your business.

Use Email Marketing

Email marketing never goes out of fashion—it remains one of the most effective ways to nurture leads and maintain client relationships. It helps keep your audience engaged and informed about the latest property listings, market trends, and real estate tips. Here’s what you need to keep in mind:

Build and segment your email list to send tailored messages to buyers, sellers, or investors.

Focus on sharing valuable, educational content rather than being overly promotional.

Use email marketing tools to automate drip campaigns and personalize your messages.

According to HubSpot, 59% of participants reported in a survey that marketing emails have an impact on their purchasing decisions. So, use this tool efficiently!

Invest in Google Ads

A well-placed Google ad can significantly enhance your visibility, as potential leads are already searching for properties on Google. By selecting the right keywords and crafting compelling ads, you can reach the right clients at the right time.

So, as long as the cost per click doesn’t drain your budget, this advertising channel is definitely worth trying.

10. Expand Your Network

In real estate, your network is your net worth. Building meaningful relationships within the industry can open doors to new opportunities, referrals, and partnerships.

Attend local networking events and engage with other business owners in your community. The more you interact, the more visible you become. And as the saying goes, visibility is profitability. If people don’t know you, they can’t do business with you.

Additionally, consider joining industry associations or real estate organizations to expand your professional network and gain access to valuable resources.

All the time and effort you put into networking can go to waste without proper follow-up. After meeting someone, make it a priority to stay in touch and nurture those connections over time.

11. Streamline Your Business Operations

Now, it's time to set up the systems and processes that will keep your real estate business running smoothly. With good operational planning, you can create a business that can grow without falling into chaos. Consider these steps:

Automate Administrative Tasks: Managing a growing real estate business involves plenty of paperwork, contracts, and scheduling. Automating tasks like invoicing and record-keeping can save time and reduce errors.

Efficient Client Communication: It is crucial to keep clients in the loop. Whether you're working with buyers, sellers, or tenants, timely and clear communication is key to building trust and ensuring smooth transactions.

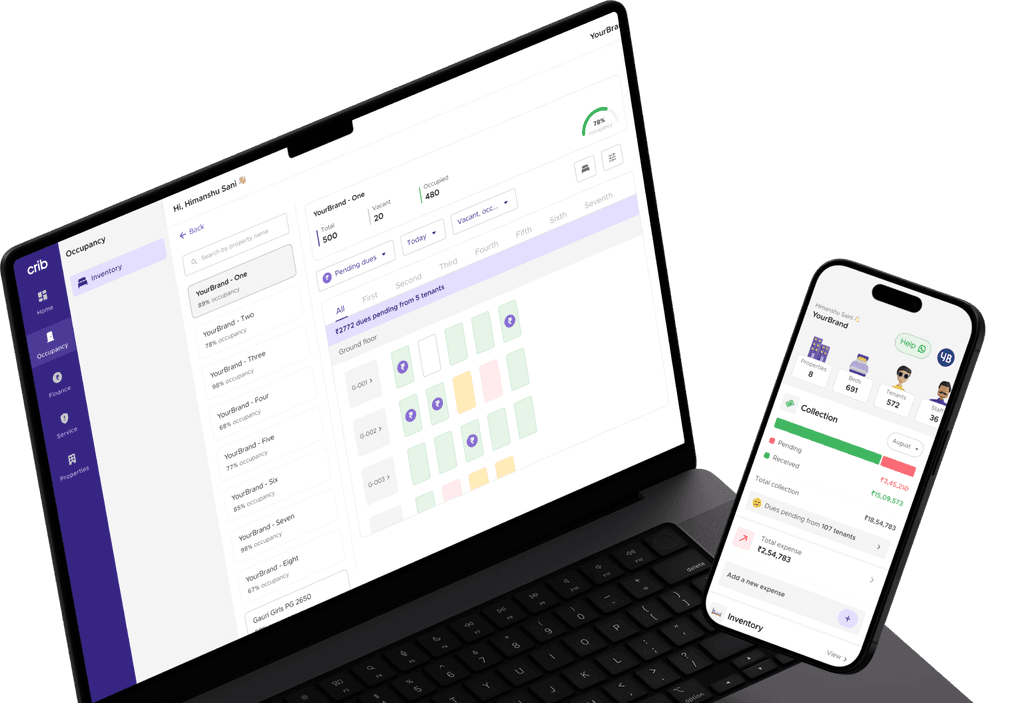

Tracking Maintenance: For property managers, staying on top of maintenance requests is essential. Property management software like Crib can help you streamline these maintenance requests for quick issue resolution and enhanced tenant satisfaction.

Standardize Process: Create standard operating procedures (SOPs) for common tasks to ensure consistency and quality in service delivery. This will help your team work more effectively and reduce training time for new employees.

Monitor Business Performance: Regularly track key performance indicators (KPIs) such as occupancy rates, rental income, and client satisfaction. Monitoring these metrics will give you an overview of your business health and help you make data-driven decisions for future growth.

By streamlining your operations and using software solutions like Crib for property management, you can focus on scaling your business without losing control over day-to-day tasks.

12. Invest in the Right Tools

The right tools can increase efficiency, streamline your workflow, and help you provide exceptional service to your clients. Depending on your specific needs, consider incorporating the following solutions:

Project Management Tools

Use tools like Trello or Asana to manage projects, assign tasks, and monitor progress. They can help you stay organized and ensure nothing falls through the cracks.

Customer Relationship Management (CRM) Tools

A CRM system like HubSpot or Zoho helps you manage client relationships, track interactions, and follow up on leads. This ensures you stay connected with your clients and provide a personalized experience throughout the sales cycle.

Property Management Tools

If you’re managing rental properties, you need comprehensive property management software like Crib. This tool automates all aspects of your operations, including payment collection, maintenance requests, tenant onboarding, and financial tracking. It helps you manage multiple properties without any stress!

Social Media Management Tools

Using platforms like Hootsuite or Buffer, you can schedule posts, track engagement, and analyze social media performance. These tools help you maintain a consistent online presence and engage with your audience across platforms like Facebook, Instagram, and LinkedIn.

Emerging Technologies

Stay ahead of the curve by incorporating emerging technologies like virtual reality for property tours, artificial intelligence for lead scoring, and blockchain for secure transactions. These innovations can enhance your services and attract tech-savvy clients.

So, this was an exhaustive guide to help you establish and scale your real estate business. While it may seem overwhelming at first, remember that you don't need to implement everything at once. Take it one step at a time, and focus on creating a strong foundation to support your long-term success.

Real Estate Business: Frequent Mistakes and How to Avoid Them

To err is human, and to learn from those mistakes is key to growth. Read on to learn about some common mistakes real estate professionals make and how to avoid them.

Making Mistakes on Social Media

Given the scale of social media, mistakes like posting outdated listings or incorrect market data are inevitable. When things go wrong, don't panic. Acknowledge the error and offer a sincere apology.

Doing It Alone

Managing every aspect of your business alone can lead to burnout. To stay efficient, delegate tasks and seek help from professionals. As you scale, bring in team members to assist you—don’t wait for mistakes to recognize the importance of collaboration.

Chasing Immediate Gains

Focusing on quick wins in real estate can be tempting, but it often neglects the importance of building lasting client relationships. Instead of just going after the next sale, take some time to nurture your existing connections. After all, real estate is more of a marathon than a sprint—so pace yourself for the long haul!

Not Investing in the Required Tools

Many people try to cut corners by avoiding investment in essential tools and technology. This leads to inefficiency and missed opportunities. Invest in CRM systems, photography equipment, property management software, and other tools to enhance your service. These tools pay for themselves by improving operations and helping you scale.

Mismanaging Finances

Many real estate businesses struggle due to inadequate financial planning and management. To avoid this, maintain detailed records, separate personal and business finances, and work with a qualified accountant. Plan for seasonal fluctuations and keep an emergency fund to cover for slow periods.

Remember, the goal isn't to be perfect – it's to learn and grow smarter.

The Bottom Line

Launching and growing a real estate business is no walk in the park. It demands commitment, hard work, and countless hours of effort. But with the right planning and smart strategies in place, you can build a flourishing business that not only achieves your goals but also surpasses your expectations.

As your real estate business grows, managing multiple properties and tenants can become increasingly complex. This is where modern property management solutions like Crib become invaluable.

Crib streamlines your operations by automating tedious tasks such as tenant onboarding, rent collection, and maintenance tracking. By simplifying these processes, Crib allows you to focus on providing exceptional service and building strong relationships with your tenants.

Crib isn’t just software—it’s a partner in your growth. In a competitive field like real estate, having a partner like Crib can help you stand out, scale faster, and stay ahead. Explore Crib—book your demo today and see the difference it can make.

Available on

All Platforms

iOS

Android

Web

download app now